In the following guest post, Thomas Boley, an associate at the Wiley Rein LLP law firm, takes a closer look at the Up-C corporate structure, and considers the claims that can arise due to the issues the corporate structure can present, as well as the insurance coverage issues that these claims may involve. Our thanks to Thomas for allowing us to publish his article as a guest post on this site. Here is Thomas’s article.

********************

The Umbrella Partnership–C Corporation structure—better known as the “Up‑C”—has rapidly evolved from a niche tax‑efficient IPO structure to a mainstream vehicle used by pre-IPO insiders seeking liquidity while preserving partnership tax treatment.[i] Over the past decade, dozens of high‑profile companies have gone public using an Up‑C, with more arriving each year as private equity funds seek exit opportunities in a strengthening IPO market.[ii]

But the same features that make Up‑Cs economically attractive may create structurally recurring dilution issues, particularly when insiders influence the use of tax distributions or the flow of liquidity between the private operating partnership and the public corporation. As recent litigation demonstrates, these structural conflicts can produce fiduciary‑duty claims against the public company’s directors and officers.[iii]

For insurers and claims professionals, this emerging pattern poses a significant challenge. Dilution‑based claims often involve shareholder class actions seeking relief directly for public stockholders.[iv] This article explains the Up‑C structure, common dilution issues arising from it, and the merits and coverage-related issues insurers should expect as more of these cases reach the pleading and settlement stages.

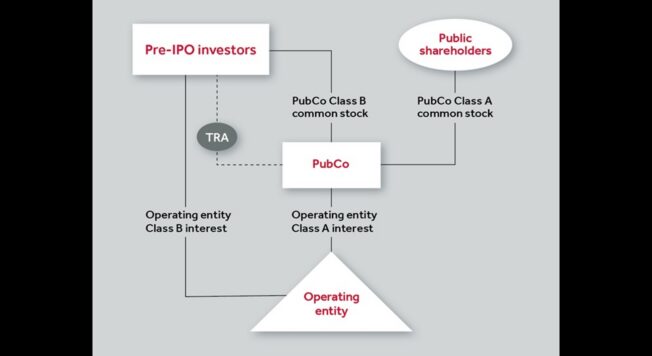

The Up-C Structure

The Up‑C structure is designed to allow pre‑IPO owners of a partnership (typically an LLC taxed as a pass‑through entity) to take a company public without converting the business into a taxable corporation. At IPO, the original owners retain units in the operating partnership (“OpCo”), while public investors purchase shares in a new C‑corporation (“PubCo”). PubCo in turn holds an interest in OpCo equal to the number of its outstanding Class A shares, while pre-IPO owners continue to own units of the OpCo.

This structure offers several benefits to pre-IPO owners. First, it preserves pass-through taxation, allowing pre-IPO owners to continue to receive pass-through treatment on OpCo income, avoiding corporate-level taxation.[v] Second, pre-IPO owners often hold Class B or similar high-vote stock in the PubCo, enabling them to retain control.[vi] Third, pre-IPO owners can exchange their OpCo units for PubCo Class A shares on a one-for-one basis, permitting pre-IPO investors to sell their interest on the public market.[vii] And fourth, pre-IPO owners typically benefit from tax receivable agreements. Under these agreements, the PubCo typically agrees to pay pre-IPO owners a percentage of the tax savings, often 85%.[viii]

Central to the Up-C’s framework is the core principle that one OpCo unit should be economically equivalent to one share of PubCo Class A stock.

Common Dilution Issues

Up‑Cs are potentially prone to dilution conflicts because of their dual‑entity design and the number of decisions that affect economic parity between the OpCo units and PubCo shares. The Up-C structure inherently divides investors into two groups: (a) public stockholders who hold Class A shares in the PubCo and (b) insiders who hold partnership interests in the OpCo and often high-vote stock in the PubCo. As insiders may dominate the PubCo’s board, decisions affecting economic parity between insiders and public stockholders, no matter how well-founded, may nevertheless create plausible fiduciary-duty claims. Examples include:

1. Trapped Cash Claims

Because the OpCo is taxed as a partnership, it must make pro rata tax distributions to all unitholders, including the PubCo, based on the highest marginal tax rate any unitholder might face. As a result, the PubCo often receives more cash than necessary to cover its own taxes (as pre-IPO individuals often have higher tax rates than corporations). That excess cash is sometimes retained by the PubCo, used to fund corporate operations, used to repurchase Class A shares or OpCo units, or held without being distributed.

If the PubCo retains substantial excess tax distributions without issuing dividends to Class A holders, then book value will increase, which may inflate the PubCo stock’s trading price. This reflects cash that is effectively attributable to public stockholders, even though they cannot access it directly. After insiders exchange OpCo units for PubCo shares and sell those shares, they may realize value derived from that trapped tax distribution after already receiving a benefit from their own tax distribution. This is the “double‑dip” theory alleged in Shumacher v. Mariotti, et al., No. 2022-0051-PAF (Del. Ch.).[x]

2. Share Buyback Claims

Another dilution dynamic involves the PubCo’s using its cash to engage in a stock buyback. In a buyback in the Up-C context, the PubCo must void an OpCo unit for every PubCo Class A share that it repurchases. This is because each Class A share in the PubCo is tied to a corresponding number of units in the OpCo. This necessarily increases the proportion of OpCo units held by insiders compared to the number held by the PubCo. At the same time, the insiders’ control over the PubCo increases if the PubCo repurchases shares from public stockholders.

This is the core theory alleged in Iron Workers Local No. 55 Pension Fund v. Viola, No. 2025-0058-JTL (Del. Ch.): public‑company cash allegedly funded repurchases that disproportionately benefited insiders.[xi] Specifically, in this case, the plaintiff alleges that the repurchase program diverted over $500 million in value[xii] from public stockholders to insiders through the asymmetrical effect of insiders’ receiving both direct cash distributions and the valuation uplift from PubCo’s repurchase of Class A shares.

In June 2026, Vice Chancellor Laster denied the motion to dismiss in this case.[xiii] Ruling from the bench, VC Laster opined that the repurchase mechanism creates an “elementary diversion of value from the public stockholders to the insiders.”[xiv]

3. Up-C Reorganizations

A third dilution‑based theory arises when an Up‑C restructures into a traditional C‑corporation (or otherwise reorganizes its capital structure) in a manner that increases insiders’ voting power without changing the nominal share count held by public stockholders. In these transactions, insiders often exchange OpCo units for high‑vote PubCo shares or receive a greater percentage of super‑voting stock than they would have obtained through a pro rata exchange. Although public stockholders may retain the same number of Class A shares, their collective voting power can be materially reduced. Plaintiffs alleged this theory in Siegel v. Cantor Fitzgerald, No. 2024-0146-LWW (Del. Ch.).[xv]

D&O Insurance Implications of Up-C Dilution Litigation

These dilution theories carry distinct implications for D&O insurance because they challenge conventional assumptions about who was harmed, what constitutes loss, and how relief is structured. Consequently, coverage questions arise that affect defense costs, allocation, and settlement posture. Several of the most significant D&O issues are discussed below.

1. Direct or Derivative

In Up‑C dilution cases, plaintiffs frequently characterize the alleged harm as direct, asserting that public Class A stockholders—not the corporation—suffered the economic injury.[xvi] Courts have reached mixed results on this characterization, and the issue is often litigated as a threshold matter.[xvii] Even where defendants ultimately succeed in re‑characterizing the claims as derivative, the costs incurred to brief and adjudicate the issue at the outset can be substantial.

The direct‑versus‑derivative distinction also materially affects defense-cost exposure and litigation leverage. When claims proceed as direct actions, they bypass demand requirements, are not subject to termination by a special litigation committee, and often avoid early application of business‑judgment‑rule deference. As a practical matter, this procedural posture can make it more difficult for defendants to secure dismissal at the pleading stage, thereby prolonging litigation and increasing defense‑cost burn before the merits are ever addressed.

2. Capacity Issues

The Up‑C structure regularly places insiders in dual roles: as equity holders of OpCo and as controllers or fiduciaries of PubCo. Because benefits may flow to insiders in both capacities, Up‑C dilution litigation frequently raises insured‑capacity issues when officers or directors are named as defendants. Insurers may contend that certain alleged conduct—such as decisions tied to OpCo ownership—was undertaken in a non‑insured capacity, giving rise to allocation disputes between covered and non‑covered loss.

These capacity distinctions also bear directly on the standard of review applied to the underlying fiduciary‑duty claims. Where plaintiffs plausibly allege that insiders used their PubCo control to advance interests tied to their OpCo ownership, courts may be less willing to apply business‑judgment‑rule deference and more inclined to review the challenged conduct under the entire‑fairness doctrine.

Entire‑fairness review materially increases litigation risk and settlement pressure, often resulting in larger resolutions than would have occurred under business‑judgment review. From a coverage standpoint, this dynamic is significant: actions taken by insiders in an arguably non‑insured capacity may nonetheless influence the applicable standard of review and the ultimate settlement value, setting the stage for aggressive allocation disputes as insurers seek to parse covered fiduciary conduct from non‑covered ownership‑level activity.

3. Settlement Characterization Risk

Up‑C dilution cases present heightened settlement‑characterization risk because the relief sought—and often obtained—may take the form of equity‑based corrective measures, rather than traditional cash payments. Plaintiffs in these matters often frame the alleged harm, not as pecuniary loss suffered by the corporation, but as differential treatment between public stockholders and OpCo unitholders that distorted economic or voting parity. As a result, settlements may be structured to “fix” the asserted imbalance instead of compensating for out‑of‑pocket damages. Where a settlement reallocates equity interests without a clear depletion of corporate assets, disputes may arise over whether the insured entity has incurred a covered “Loss” at all.

This characterization issue is particularly acute in Up‑C litigation because the alleged injury is often relational—that is, rooted in relative ownership percentages, voting power, or access to liquidity—making it more difficult to anchor settlement value to a traditional damages model. As a result, a settlement’s characterization of the dispute may be subject to engineering designed to create or expand coverage, giving rise to consent‑to‑settle complications, particularly where allocation issues already exist.

4. Repeat-Player Risk

For insurers, Up‑C dilution litigation presents a repeat‑player risk rather than a one‑off exposure. The same structural features—tax distributions, exchange rights, and control‑preserving governance—remain in place indefinitely. The design features of Up-C corporations necessarily lend themselves to dilution-based claims and ratable-benefit claims based on inherently different treatment of OpCo unitholders and PubCo public stockholders.

As Up-C litigation can center around issues regarding structural and inherent features of the corporate structure, issues concerning fortuity and prior acts exclusions may also play a role in evaluating coverage.

Practical Guidance for Insurers and Claims Professionals

As Up‑C dilution litigation continues to expand, insurers and claims professionals should expect resulting litigation to become a recurring feature of the D&O landscape and take steps to anticipate the unique risks they present. Underwriters should carefully examine whether a prospective insured uses an Up‑C structure. Because Up‑C litigation often turns on allegations that insiders failed to maintain economic parity between public shareholders and pre-IPO insiders, insurers may wish to consider endorsements or clarifications addressing parity‑related demand and harms, which may prove to be unavoidable consequences of the Up-C structure or take other measures to address the inherent risk posed by this corporate structure.

[i] PwC, Considering an IPO? Here’s why an Up-C might be advantageous, Observations from the front lines, https://www.pwc.com/us/en/services/consulting/deals/library/up-c-structure.html (last visited June 9, 2026).

[ii] Treston Morrow et al., Up-C Structured IPOs, IPO Preparation (Aug. 11, 2022), https://www.ipohub.org/article/up-c-structured-ipos.

[iii] See Complaint at 33, Shumacher v. Mariotti et. al, No. 2022-0051-PAF (Del. Ch. June 2, 2022), Dkt. No 35; Complaint ¶ 16, Iron Workers Local No. 55 Pension Fund v. Viola et. al., No. 2025-0058-JTL (Del. Ch. Sep. 15, 2025), Dkt. No. 28.

[iv] Id.

[v] Debevoise & Plimpton, The Up-C Goes to Court: Managing the Emerging Risks of an Advantageous Tax Structure, Insights & Publications (May 2023),https://www.debevoise.com/insights/publications/2023/05/the-up-c-goes-to-court.

[vi] Id.

[vii] Id.

[viii] Id.

[ix] Id.

[x] Verified Am. Class Action Complaint, Schumacher v. Mariotti, et al., No. 2022-0051-PAF (Del. Ch. Jun. 2, 2022).

[xi] Complaint, Iron Workers Local No. 55 Pension Fund v. Viola et. al., No. 2025-0058-JTL (Del. Ch. Sep. 15, 2025), Dkt. No. 28.

[xii] Id.

[xiii] Jarek Rutz, Virtu Insider Buyback Suit Survives Dismissal Bid, Law360, Jun. 2, 2026, https://www.law360.com/articles/2484380/virtu-insider-buyback-suit-survives-dismissal-bid

[xiv] Id.

[xv] Opinion, Siegel v. Cantor Fitzgerald, L.P. et al., No. 2024-0146-LWW (Del. Ch. Apr. 10, 2025), Dkt. No. 53.

[xvi] See, e.g., Compl., Iron Workers, No. 2025-0058-JTL (Del. Ch. Sep. 15, 2025), Dkt. No. 28.

[xvii] Compare Shumacher and Siegel. See also Iron Workers Tr. at 69–70 (suggesting that theoretically shareholder buyback claims should be direct under Tooley, but due to Brookfield’s bright line approach, assuming that it’s derivative).