On April 15, 2020, OECD released the report titled “Tax and Fiscal Policy in Response to the Coronavirus Crisis: Strengthening Confidence and Resilience” (the “COVID-19 Response”). The COVID-19 Response discussed the decisive action many governments have taken to contain and mitigate the spread of the virus and to limit the adverse impacts on their citizens and their economies, and outlined various tax policy options as available tools. Included in the tax policy discussion is the commitment to stay the course in response to the tax challenges of the digitalisation of the economy and ensuring that MNEs pay a minimum level of tax. (p.6) In the COVID-19 environment, the new impetus to efforts to reach agreement on Pillar One issues internationally can now stem not only from “[t]he increased use of digital services” but also from “the need to collect more revenues” which can be achieved, in part, by “strengthening the taxation of economic rents” (p.6) particularly of the companies which perform relatively well during the crisis.

The intent to focus the “taxation of economic rents” on better-performing enterprises has been reinforced in the OECD’s “Statement on a Two-Pillar Solution to Address the Tax Challenges Arising From the Digitalisation of the Economy” published on July 1, 2021 which proposes that in-scope companies be defined as the MNEs with global turnover above 20 billion euros and profitability above 10%. While the profit margin cut-off may seem reasonable, the one-size-fits-all approach is disheartening.

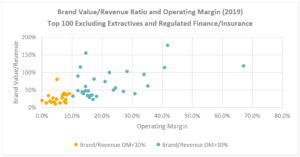

A quick review of the top 100 brands valued by BrandFinance[1] illustrates the point: while for the companies with operating margins under 10% the ratios of brand value to revenue cluster between about 15% and 40%, for companies with operating margins in excess of 10% – which companies would be in-scope as proposed by the Statement – the ratios of brand value to revenue are spread widely between 20% and over 100%. Thus, if the 10% profitability were to be accepted as a simple mechanical threshold, the residual profits that would be subject to allocation as Amount A could include, in part, the return on the MNE’s brands. One can question whether this is OECD’s intention.

[1] brandirectory.com/global Brand Finance Global 500 January 2020