Since July 2022 when the FCA published its rules and guidance to implement the Consumer Duty, much ink has been spilled on what it will mean for affected firms. Now, with the clock ticking down to implementation on 31 July 2023, the FCA has published the findings of its review of a number of larger firms’ plans for complying with the Duty.

“Could do better” is the overall mark on the industry’s homework so far.

What will the Consumer Duty involve?

To recap, the reforms will involve:

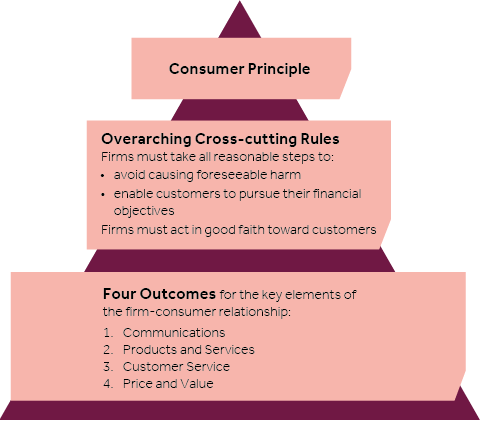

- An overarching Consumer Principle requiring firms to act to deliver good outcomes for retail customers when selling products and services.

- Cross-cutting rules providing clarity on FCA expectations, which will require firms to act in good faith, avoid causing foreseeable harm, and enable and support retail customers to pursue their financial objectives.

- Rules relating to the four outcomes the FCA wants to see, around: appropriateness of products and services; transparent pricing and fair value; consumer understanding; and consumer support.

The Consumer Duty will apply to all firms that sell products and services to retail customers. It will cover a wide range of products and services, including investment and pension products, insurance products, and consumer credit.

The implementation review

In its review findings, the FCA has called out (unnamed) firms that are behind on their preparations for the Consumer Duty and has warned that they risk falling foul of the new rules when the come into force. The FCA has emphasized that firms must be proactive in ensuring that they will meet the Consumer Duty requirements when the time comes. It has expressed some concern that the plans of some firms are superficial, and represent a degree of overconfidence that existing policies and processes will be adequate. It also highlighted the need for firms to work together with other firms in their distribution chains, an area the FCA felt was neglected in some firms’ planning.

As ever, the FCA says it will take a risk-based approach to enforcement, focusing its attention on firms that pose the greatest risk to consumers, in its view. Similarly, it is urging firms to prioritize, and focus on assessing where they are least likely to be satisfying the requirements of the Consumer Duty, and seeking to reduce those worst risks of poor consumer outcomes.

The FCA has also provided some further clarity on aspects of the new rules, stating that firms must take a holistic approach to assessing the value of their products and services. This includes considering the costs, benefits, and risks associated with each product or service, as well as how well the product or service meets the needs of the consumer. The FCA expects firms to be transparent in their pricing and communicate clearly with consumers about the costs and benefits of each product or service. The FCA expects this to be embedded in the culture of firms and the subject of sufficient governance and oversight focus and resourcing – all areas in which the FCA felt some firms’ plans to date have lacked detail.

Lastly, the FCA stressed that firms need to consider the types and granularity of data required to monitor compliance with the Consumer Duty, and not just assume it will be sufficient to repurpose existing data gathering.

Raising the bar

The FCA has repeatedly emphasized that the Consumer Duty is intended to represent a raising in standards of consumer protection in the UK financial services sector. The Duty can be expected to bring with it a heightened level of accountability on firms for ensuring good customer outcomes (as the FCA views them). It says it will work closely with financial firms to support them in implementing the Consumer Duty and is providing a variety of guidance and support. This includes guidance on how to carry out customer need assessments, how to provide clear information about products and services, and how to assess the affordability of products and services.

On the other hand, the FCA says will take appropriate action against firms that fail to comply with the new rules. Where meaningful customer harm is found post-implementation, firms can no doubt expect to face significant penalties, as well as reputational damage, which could impact their ability to operate effectively in the future.