Introduction

On May 3, 2023, the United States Tax Court held in ES NPA Holding, LLC v. Commissioner, T.C. Memo. 2023-55, that the taxpayer’s receipt of interests in a partnership in exchange for services rendered to the sole owner of the business before it became a partnership was for the benefit of the future partnership and, therefore, was a profits interest (rather than a capital interest). The taxpayer did not provide ongoing services to the partnership.

The case is also a reminder that, in order for an interest to qualify as a profits interest, upon a hypothetical sale of the partnership’s assets and distribution of the proceeds in liquidation immediately after the interest is issued, the recipient must not receive any value. Therefore, the value of the partnership assets is important, and the IRS may challenge the value of the assets.

Because the case is merely a memorandum opinion, it has no precedential value. Still, it does provide an indication on how at least one Tax Court judge would approach the issues. It is also unclear whether the IRS will appeal the case and whether the Court of Appeals for the Eighth Circuit would uphold it.

Summary of the Case

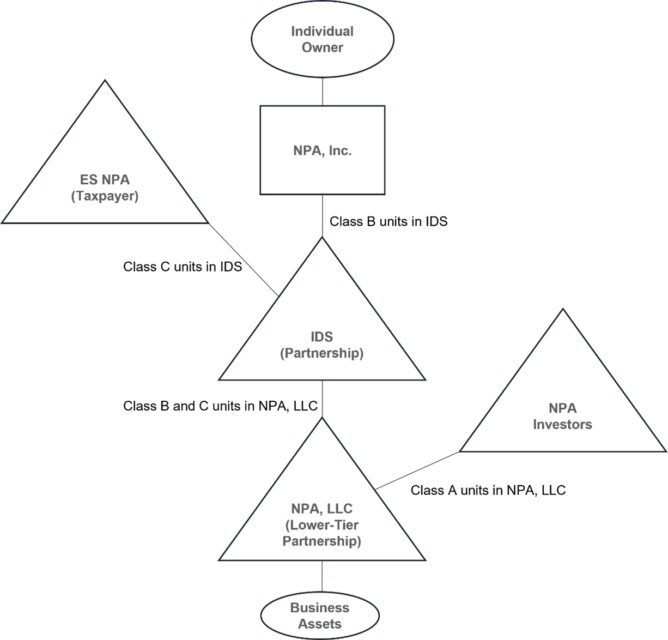

NPA, Inc. sought to sell a portion of its internet-based consumer loan business. NPA, Inc. retained ES NPA Holding, LLC (the “Taxpayer”) to help NPA, Inc. assemble an investor group to purchase 40% of NPA, Inc.’s business. The Taxpayer also provided strategic advice to NPA, Inc. on the operation of the business after it became a partnership. This turned out to be key.

In exchange for these services to NPA, Inc., the Taxpayer received an option to purchase all class C units in an upper-tier partnership – Integrated Development Solutions, LLC (“IDS” or the “Partnership”) – that, after the investor group purchased an interest in the business, would hold an interest in a lower-tier partnership, NPA, LLC (the “Lower-Tier Partnership”), that would operate the consumer-loan business.[1]

At the end of the transaction, the Taxpayer held class C units in the Partnership. The Partnership held class C units in the Lower-Tier Partnership. NPA, Inc. held class B units in the Lower-Tier Partnership, and the investor group held class A units in the Lower-Tier Partnership. The Lower-Tier Partnership held the business assets.

The Taxpayer treated the receipt of its class C units as the tax-free receipt of a profits interest pursuant to the safe harbor in Revenue Procedure 93-27 (the “Revenue Procedure”).

The Revenue Procedure provides that the receipt of a “profits interest” for the “provision of services to or for the benefit of a partnership in a partnership capacity or in anticipation of being a partner” is not taxable. A profits interest, in turn, is defined as any partnership interest other than a capital interest. A capital interest is an interest that would “give the holder a share of the proceeds if the partnership’s assets were sold at fair market value and then the proceeds were distributed in a complete liquidation of the partnership”.

The IRS argued that because the services were provided to NPA, Inc., they were not to or for the benefit of the Lower-Tier Partnership and, therefore, the safe harbor did not apply. The IRS also argued that, were the partnership’s assets sold at fair market value and the proceeds distributed in a complete liquidation of the Partnership, the Taxpayer would receive $12 million, and not zero. The IRS’s expert testified that, the sale of ultimately 70% of the business to the third-party investors was not at fair market value.

The Tax Court found for the Taxpayer on both points.

Although the Taxpayer had argued that any interest received in anticipation of being a partner can qualify as a profits interest (i.e., by providing services to NPA, Inc. in anticipation of being a partner with NPA, Inc.), the Tax Court clarified that the services must be provided to or for the benefit of the partnership. But it held that the partnership need not be a partnership when the services are rendered. In this case, when the Taxpayer provided its services, IDS (the entity that would become the Partnership) was merely a disregarded entity of NPA, Inc. However, because at least some of the services related to the future business of the future partnership, the Tax Court held that the requirement of the Revenue Procedure that the interest be received for the “provision of services to or for the benefit of a partnership in a partnership capacity or in anticipation of being a partner” was satisfied.

The IRS did not argue, and the Tax Court did not address the fact, that the Taxpayer provided two distinct categories of services: (i) finding investors for NPA Inc.’s 40% interest in IDS (the service which was rendered solely to NPA, Inc.), and (ii) providing strategic advice relating to the future business of the Lower-Tier Partnership. The first category of service was rendered solely to NPA, Inc. because it related to the sale of interests in IDS and not to its business.

The Tax Court dismissed the IRS’s argument that the Revenue Procedure was not satisfied because the strategic advice was rendered to the Lower-Tier Partnership, but the Taxpayer received an interest in the (upper-tier) Partnership.[2]

Having concluded that the Taxpayer rendered services for the benefit of the Lower-Tier Partnership in anticipation of being a partner, the Tax Court held that the Taxpayer potentially satisfied the Revenue Procedure.[3] It next considered whether the Taxpayer had received a profits interest, rather than a capital interest.

To determine whether the Taxpayer received a profits interest, the Tax Court analyzed whether the Taxpayer would receive any distribution upon a hypothetical sale of the Lower-Tier Partnership’s assets and distribution of the proceeds in liquidation at the time the Taxpayer received the class C units. The Taxpayer had valued the Partnership’s assets based on the amount the third-party buyers had paid for their interests. The IRS argued that the sale to third-party investors was not at fair market value but at a discount. The Tax Court (i) held that the sale was at arm’s length, (ii) accepted Taxpayer’s valuation, (iii) determined that, upon a hypothetical sale of the Lower-Tier Partnerships assets and a distribution of the proceeds immediately after the profits interest was issued, the Taxpayer would receive nothing, (iv) and held that, therefore, the interest was a profits interest.

Implications

The Tax Court read the Revenue Procedure expansively. It allowed a partnership interest to qualify under the Revenue Procedure where the services were rendered before the partnership was formed and allowed the entirety of the partnership interest to qualify as a profits interest even where some (perhaps most) of the services were rendered solely to a partner and not at all to the future partnership.

However, there was a limit to the Tax Court’s reading of the Revenue Procedure. It did insist that the services be rendered “to or for the benefit of the future partnership”.

Therefore, under the case, if the services provided by a prospective partner do not benefit the future partnership, then any profits interest received would not qualify for tax-free treatment under the Revenue Procedure.

The Tax Court also permitted the taxpayer to render services to a lower-tier partnership and receive interests in an upper-tier partnership, at least where the interests in each were identical.

The case provides a reminder that a partnership interest will qualify as a profits interest only if, immediately after the interest is issued, in a hypothetical sale of the partnership’s assets for fair market value, and a distribution of the proceeds in liquidation, the profits interest partner would receive nothing, and that the IRS may challenge valuations.

Because the case is merely a memorandum opinion, it has no precedential value. Still, it does provide an indication on how at least one Tax Court judge would approach the issues. It is also unclear whether the IRS will appeal the case and whether the Court of Appeals for the Eighth Circuit would uphold it.

[1] More specifically, immediately before NPA, Inc. issued the option to the Taxpayer, NPA, Inc. contributed its business assets to Lower-Tier Partnership in exchange for class A, B, and C units in the Lower-Tier Partnership. NPA, Inc. sold the class A units to the investor group. NPA, Inc. contributed the class B and class C units to the Partnership in exchange for “mirror” class B and C units of the Partnership. Then, the Taxpayer exercised its option and received the class C units in the Partnership.

[2] See op. cit. 12 (“It is of no material consequence that ES NPA’s [the Taxpayer’s] interest in NPA, LLC [the Lower-Tier Partnership] is held indirectly through IDS [the [upper-tier] Partnership]], which is a mere conduit since the liquidation rights in the class C units in both IDS and NPA, LLC are identical.”).

[3] The other prohibitions of the Revenue Procedure – that the profits interest cannot relate to a substantially certain and predictable stream of income from partnership assets, such as income from high-quality debt securities or a high-quality net lease, that the profits interest cannot be sold within two years of receipt, and that the profits interest cannot be a limited partner interest in a “publicly traded partnership” within the meaning of section 7704(b) of the Internal Revenue Code – were not at issue.